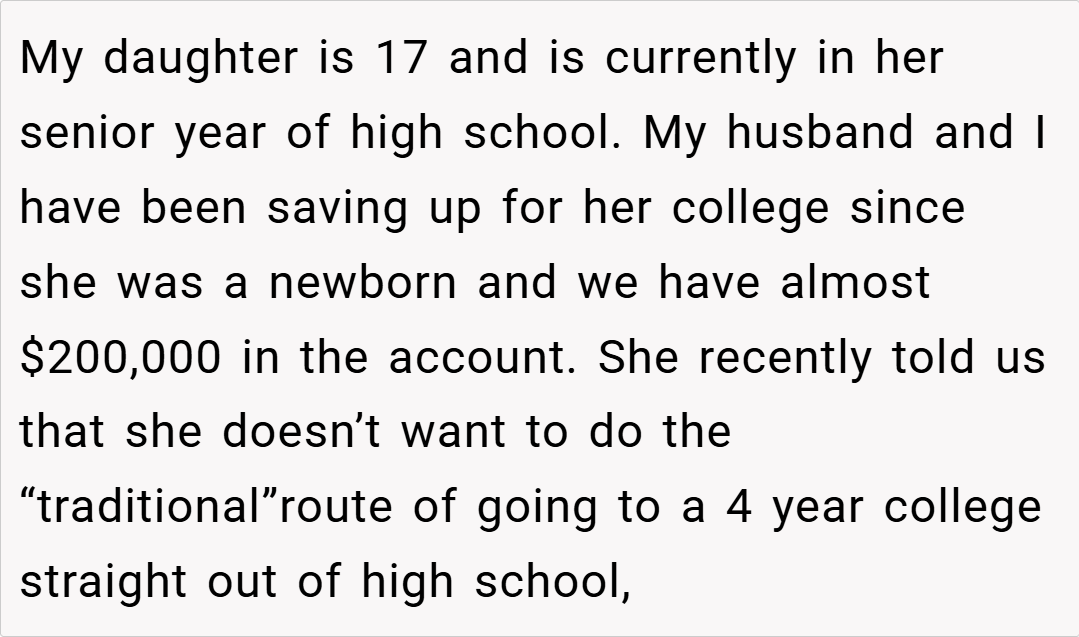

AITAH for not giving my daughter her college fund money?

Deciding how to manage a college fund can be as challenging as it is emotional—especially when your daughter’s plans diverge sharply from the traditional path you envisioned. In today’s story, a 35-year-old parent recounts the heated disagreement with their 17-year-old daughter about accessing nearly $200,000 saved for college.

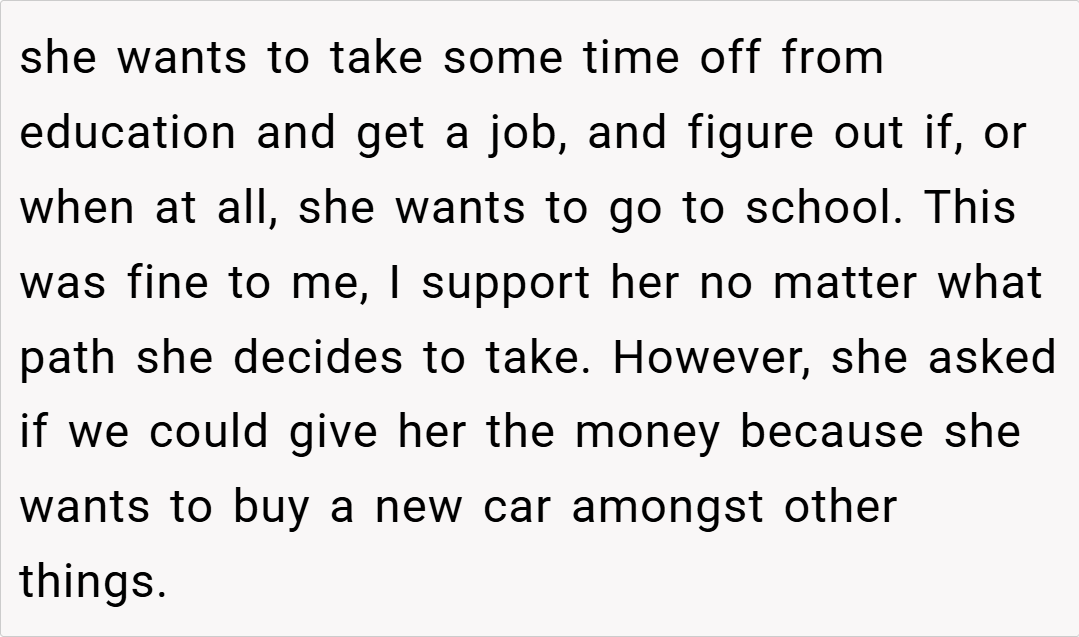

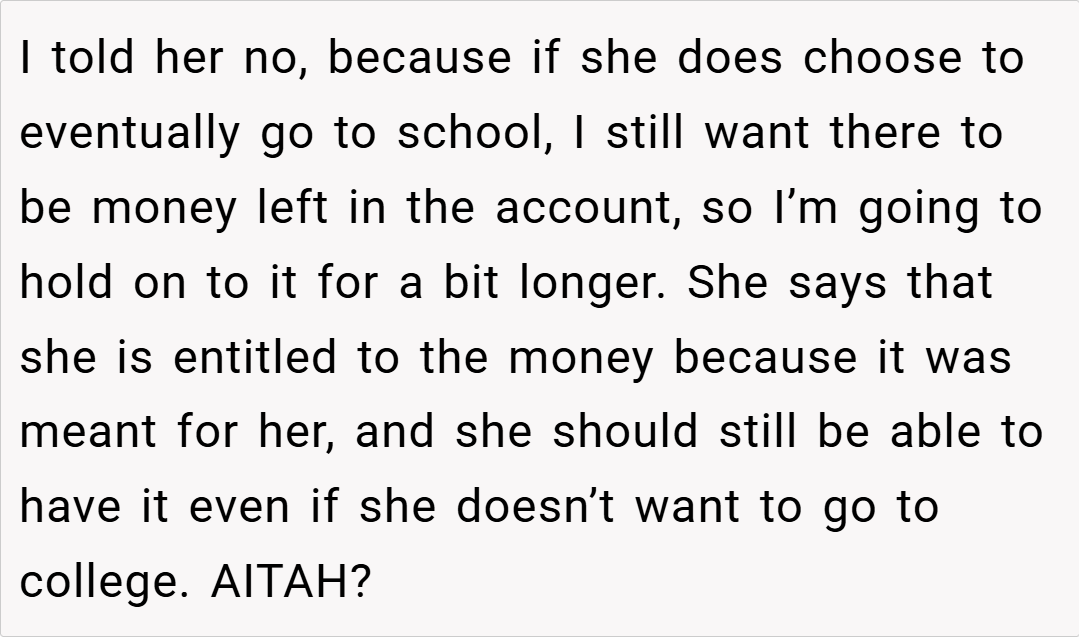

While the daughter, now a high school senior, has chosen to take a break from academics and get a job, she wants to use the money for a new car and other immediate expenses. The parent, however, insists on holding onto the funds so that there will be resources available if and when she decides to attend college later.

With both sides holding strong beliefs about entitlement and long-term planning, this situation has left the family in a bitter standoff. The tension here isn’t just about money—it’s about differing visions for the future. The parent sees the college fund as a safety net, built from years of sacrifice,

while the daughter argues that the money was always meant for her benefit, regardless of the traditional college route. As emotions run high and accusations fly, the question remains: is it unreasonable for a parent to withhold the funds, or is it a necessary precaution for securing her future?

‘AITAH for not giving my daughter her college fund money?’

Expert Opinion:

Navigating financial planning for a child’s future is a delicate balance between supporting immediate needs and safeguarding long-term goals. Dr. Laura Markham, a clinical psychologist known for her work on family dynamics and financial stress, explains, “When parents save money for education, it’s typically a hard-earned safety net intended to provide security and opportunity later on.

While it’s natural for a young person to want to use that money for other purposes, removing those funds can have long-lasting implications on future opportunities.” Dr. Markham’s insight underscores that the college fund represents not just money, but years of planning and sacrifice meant to secure a stable future.

Dr. Markham further elaborates, “Parents and children sometimes clash over money because they have different time horizons. A teenager may prioritize immediate gratification—like buying a car—while a parent focuses on long-term benefits such as higher education.

In these cases, a compromise, such as allowing a partial withdrawal with conditions, might be ideal, but it depends on mutual trust and clear communication.” Her perspective suggests that while the daughter’s desire is understandable, the parent’s insistence on preserving the fund is equally valid given the uncertainty of future academic decisions.

Relationship and financial expert Dr. John Gottman also weighs in on the broader implications. “Financial disagreements in families often reflect deeper differences in values and risk tolerance,” he states. “When a child challenges a long-term savings strategy with immediate wants, it is crucial to address the emotional aspects behind that request.

A college fund is not just about education—it’s about ensuring that unforeseen challenges do not derail future plans.” According to Dr. Gottman, the key is fostering dialogue where both parties understand that the decision is less about control and more about protecting the child’s future security.

His advice echoes the need for patience and compromise, even if the initial stance might seem harsh to a young person eager for independence. Both experts agree that these kinds of conflicts highlight the importance of setting clear expectations early on.

The parent’s approach, though it may feel bitter to the daughter, is a pragmatic decision based on decades of careful saving and the unpredictable nature of life. While the daughter may feel entitled to access the money immediately, the long-term security that the fund provides is a cornerstone of responsible financial planning for higher education—a commitment the parent has made over many years.

See what others had to share with OP:

Several redditors expressed strong support for the parent’s decision. One user commented, “After saving for years, that college fund isn’t just cash—it’s a safety net for your future. It’s completely fair to insist on keeping it intact, even if your daughter doesn’t want to follow the traditional route.”

Another group shared personal stories of financial disagreements in their families, with one commenter saying, “I get it—when you’ve worked hard to save for college, you want those funds to be there when you really need them. Your daughter might think she’s entitled to it now, but you’re just being responsible.”

In the end, insisting on holding onto the college fund is not about being stingy—it’s about ensuring a secure future for your daughter, even if her plans don’t align with the traditional path. The disagreement encapsulates a broader issue of balancing immediate desires with long-term security.

While the daughter’s request for access to her college fund reflects a desire for independence, the parent’s refusal is rooted in years of careful planning and the hope that she will eventually benefit from higher education. This case forces us to ask: How do we balance the allure of immediate gratification with the importance of long-term planning?

What would you do if your future was at stake by compromising a hard-earned safety net? We invite you to share your thoughts and experiences: Have you ever faced a similar financial conflict with a family member?

Do you believe that personal entitlement should override long-term planning, or is patience and foresight the key? Let’s discuss how we can navigate these tricky waters of family finances and personal independence.