AITA for creating a safe account for my wife?

Family finances are often the subject of deep-seated expectations and painful legacies. In this story, a 38-year-old man from India reveals the fallout after he created separate safe accounts for his wife and children.

Inspired by his own tumultuous past—marked by his father’s transformation after a life-changing accident and the sacrifices his mother made to keep the family together—he wanted to ensure his wife, Eve, would never feel trapped or financially pressured, especially after she chose to stay home with their newborn twins. Despite building up these accounts to near six figures, a vacation mishap exposed his secret planning, igniting familial fury and forcing him to question if his protective actions make him the asshole.

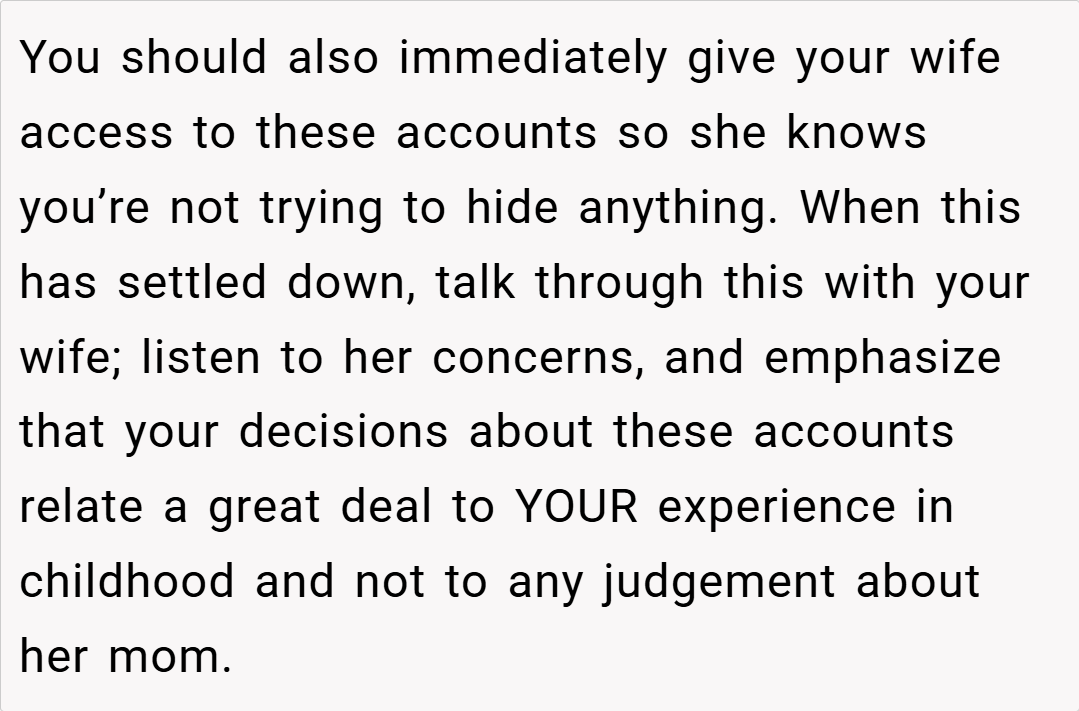

The confrontation escalated when his younger sister and mother, upset by his withholding of funds, demanded that he share the money. While his older sister supported his decision, his wife is now torn, suggesting the money should instead go to their children or even his mother. With heavy hearts and clashing values, he now wonders if choosing to protect his wife’s autonomy and security was the right call.

‘ AITA for creating a safe account for my wife?’

Expert Opinion:

Dr. Laura Markham, a clinical psychologist specializing in family dynamics and financial stress, states, “Financial safeguards in a family are not just about money—they are about preserving autonomy and preventing future emotional and financial hardship. When a parent creates secure accounts to protect a partner from potential abuse or neglect, it’s an investment in long-term emotional well-being rather than a snub to traditional family expectations.”

She adds, “It is crucial to understand that not all financial decisions are meant to please every family member. In cases where there is a history of painful sacrifice, such measures are necessary for safeguarding the individual’s future.” Her perspective underscores that the husband’s actions are a reaction to a legacy of hardship—a legacy he vowed to protect his wife from at any cost.

Relationship expert Dr. John Gottman also emphasizes, “Boundaries in financial planning, especially in families with complex histories, are vital. When a partner takes proactive steps to create a safety net, it reflects a deep commitment to preventing the repetition of past traumas. The backlash from other family members, while painful, often stems from unresolved expectations about wealth and support.”

Dr. Gottman notes that in blended families, particularly where cultural and generational gaps exist, it is common for older relatives to cling to traditional notions of financial responsibility. “The key is open communication,” he advises. “Even if the actions seem harsh, they are often rooted in the desire to break free from an oppressive cycle and build a future based on personal happiness and mutual support.” Both experts agree that while the decision may ruffle some family feathers, it is a valid and necessary step toward protecting emotional and financial autonomy.

Check out how the community responded:

Several redditors voiced their support for his decision. One commented, “You have every right to create a safety net for your loved ones. Family legacy is important, but not at the expense of your partner’s independence and well-being.” Many echoed that protecting one’s future shouldn’t be compromised by outdated expectations.

Another group shared personal experiences of breaking away from traditional financial control. One user remarked, “I’ve seen families where one person’s financial planning was seen as secretive or selfish. In reality, it’s about preserving your peace of mind. Your choice is both brave and responsible.”

Ultimately, your decision to create separate accounts for your wife and children was a measure of self-protection and love—a way to ensure that your wife would never have to endure the hardships you experienced.

While it may have upset some family members who expect to be included in your financial decisions, choosing your own happiness and security over traditional expectations is not only understandable but commendable. This case forces us to ask: How do we balance familial obligations with personal autonomy and emotional well-being?

What would you do if you were faced with a similar choice between tradition and protecting your loved ones? Share your thoughts and experiences below—your insights might help others navigate the delicate balance between family legacy and individual self-respect.

You worked for that money, and you do want you want with it. Your wife is just hurt and angry right now – do not count her out right now. Keep the account open somehow for her and your children. set up a trust with a lawyer and keep sister and mom out of the discussion.