AITA for lashing out on my stay-at-home husband for spending our household budget on my SIL whom I despise ?

When finances and family dynamics collide, even the smallest expenditures can spark a wildfire of emotions. In this story, a 33-year-old woman—a sole breadwinner supporting her stay-at-home husband and two-year-old daughter—found herself fuming when her husband used part of their monthly household budget on his sister-in-law, a person she truly despises.

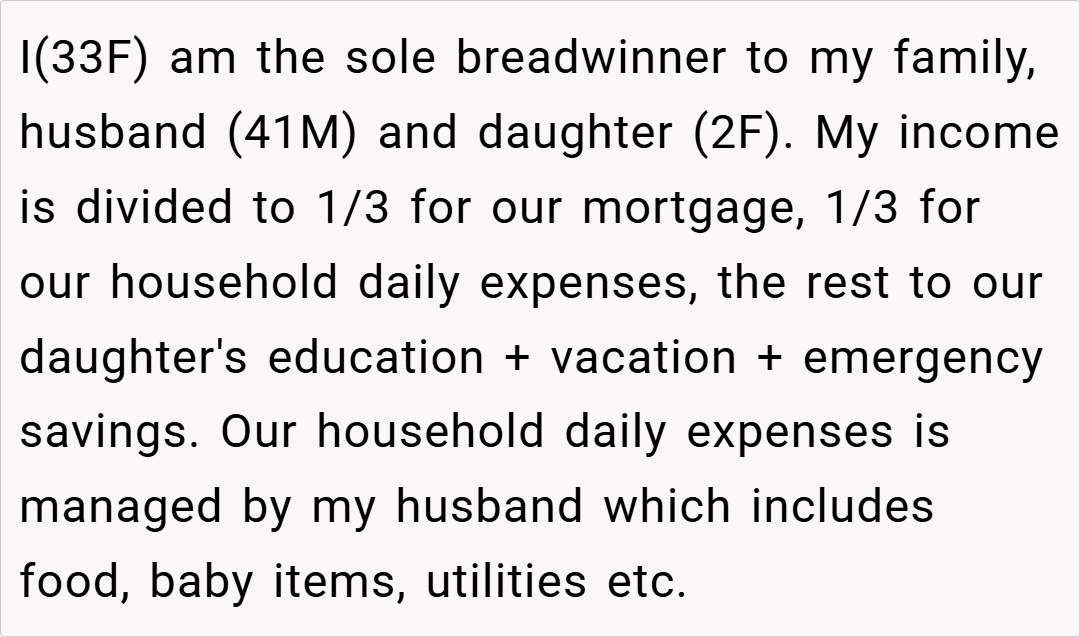

With a strict budget allocated for essentials and a careful plan for their daughter’s future, she felt that his spending habits, especially on non-essential items like gifts for his SIL and alcohol, threatened the stability she worked so hard to maintain.

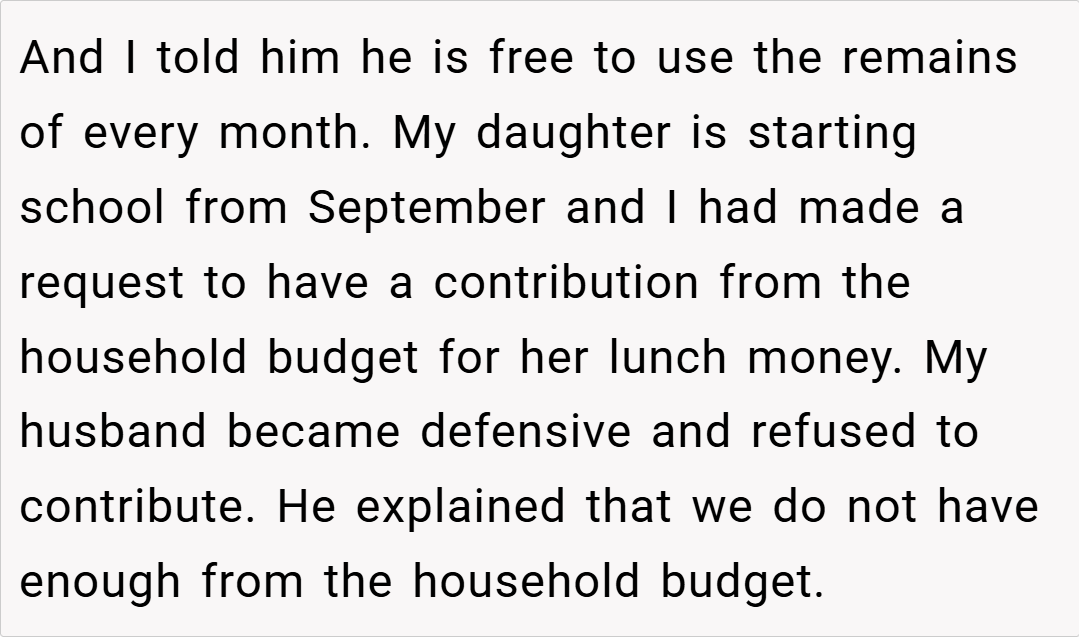

Her frustration boiled over when her husband refused to contribute to their daughter’s new school lunch fund, claiming they simply didn’t have enough money. In a moment of heated emotion, she lashed out about his spending choices. But is her reaction justified—or did she overstep by targeting his discretionary spending?

‘ AITA for lashing out on my stay-at-home husband for spending our household budget on my SIL whom I despise ?’

Letting emotions spill over in financial disagreements is more common than many realize. Dr. Emily Richardson, a relationship and financial counselor, notes, “Disagreements over money can reveal deeper issues of control and respect in a relationship. It’s important for both partners to have clear, mutually agreed-upon financial boundaries.”

She explains that when one partner is given free rein over a budget—especially one meant to cover family essentials—it can lead to frustration if unexpected expenses arise. In this case, the request for additional school lunch money represents a non-negotiable need that should be met before discretionary spending.

Dr. Richardson further advises, “In households where one partner handles day-to-day finances, transparent communication is key. Couples should periodically review spending priorities together. This prevents resentment from building when one partner’s choices—such as spending on alcohol or gifts—conflict with family necessities.”

She believes that, ideally, both partners should contribute to a joint financial plan that accounts for both fixed expenses and discretionary funds, ensuring that no one feels financially overburdened or controlled.

She also emphasizes that emotional outbursts, while understandable, often indicate underlying issues that need addressing. “When a partner lashes out, it’s a signal that they feel unheard or that their priorities are being undermined.

It’s crucial to use these moments as opportunities for constructive dialogue rather than as battlegrounds for blame.” In this instance, her outburst about his spending habits was a cry for a more balanced approach to managing their finances, especially given the importance of saving for their daughter’s future.

Additionally, Dr. Richardson highlights that spending habits often carry emotional weight. “If one partner feels that the other is misusing funds—particularly for items that seem frivolous—it can trigger feelings of betrayal or neglect.

This is not simply about the money; it’s about ensuring that every dollar contributes to the family’s long-term security.” Her advice is clear: schedule a serious discussion about finances, possibly with the help of a mediator or financial planner, to rebuild trust and establish a fair system that respects both partners’ contributions.

Here’s the comments of Reddit users:

Overall, the community is split on the issue. A significant number of redditors agree that the OP’s frustration is justified because her husband’s discretionary spending on his sister-in-law—especially when it impacts funds earmarked for their daughter’s needs—signals a lack of shared financial responsibility.

These commenters emphasize the importance of clear, joint budgeting and say that her outburst was a necessary wake-up call to address financial mismanagement. However, a contrasting viewpoint argues that if the money is truly “free” to spend after covering essentials, then micromanaging how he chooses to use it may be overstepping.

Some believe that establishing a regular allowance for discretionary spending could have been a more balanced approach, rather than resorting to lashing out. In essence, while many sympathize with her concern for their daughter’s future, others feel that her response crossed a line by trying to control his personal spending habits.

Let’s look at this like business. Your family is your business

Your child is an asset of that business. As assets age cost to maintain will increase and unless there is an increase in revenue the existing needs to be evaluated to determine where funds can be redistributed to account for the increase in maintenance. Lunch money this year, as the years move on there will be added expenses for sports or dance or band. Looking at the long term if your revenue doesnt increase at the same rate what happens then? Can you refinance to a lower rate on your mortgage? Do you have car payments? How much longer until that’s paid off?

I would take my next paycheck and open a new bank account, set up all bills on autopay, and a bank transfer monthly to old bank account for husbands allowance. Then set up a monthly discussion on expenses to make any adjustments.