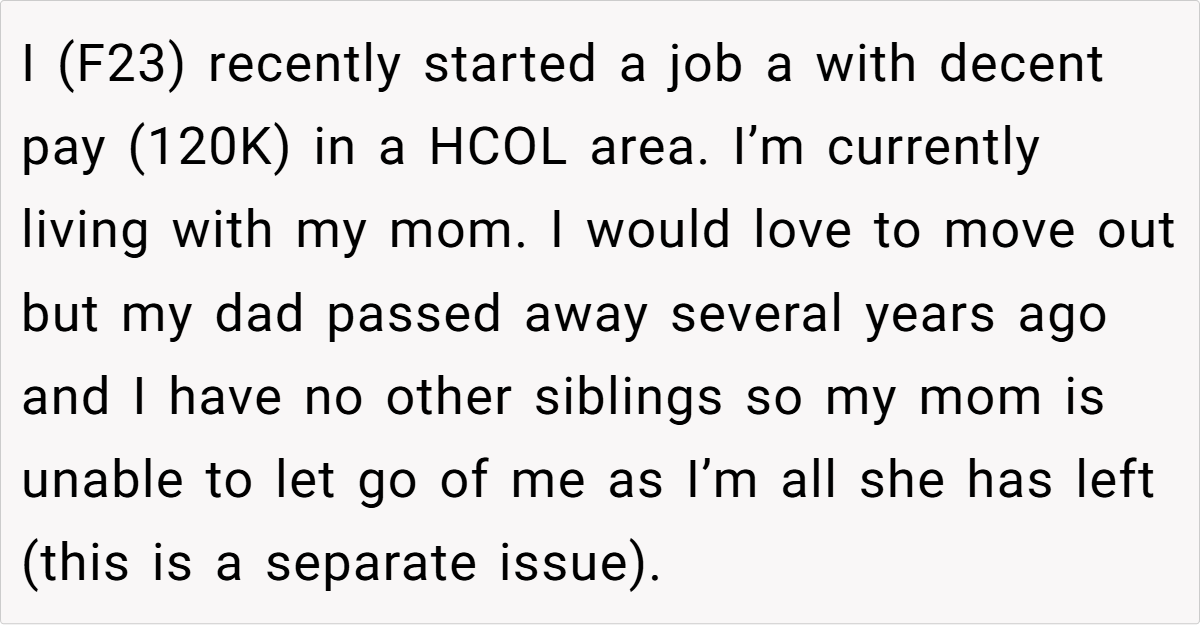

WIBTA if I don’t give my mom an “allowance” now that I have a job?

Living in a high-cost-of-living area while supporting a parent can create an emotional tug-of-war between love and financial practicality. In this story, a 23-year-old woman who recently landed a well-paying job finds herself caught in a dilemma: her mom, who is financially secure yet emotionally attached, insists on receiving a monthly “allowance” of $1,000.

This money isn’t used to improve her quality of life but rather serves as a status symbol for bragging rights. The tension lies not only in the dollars but in the deep-seated need for validation, creating an uncomfortable mix of gratitude, guilt, and frustration.

For our storyteller, the request feels more like an unnecessary financial drain than a gesture of care. Balancing the desire to support a parent with the need to safeguard her own future, she now wonders if halting these payments is justified. The situation raises important questions about where emotional obligation ends and personal financial responsibility begins.

‘WIBTA if I don’t give my mom an “allowance” now that I have a job?’

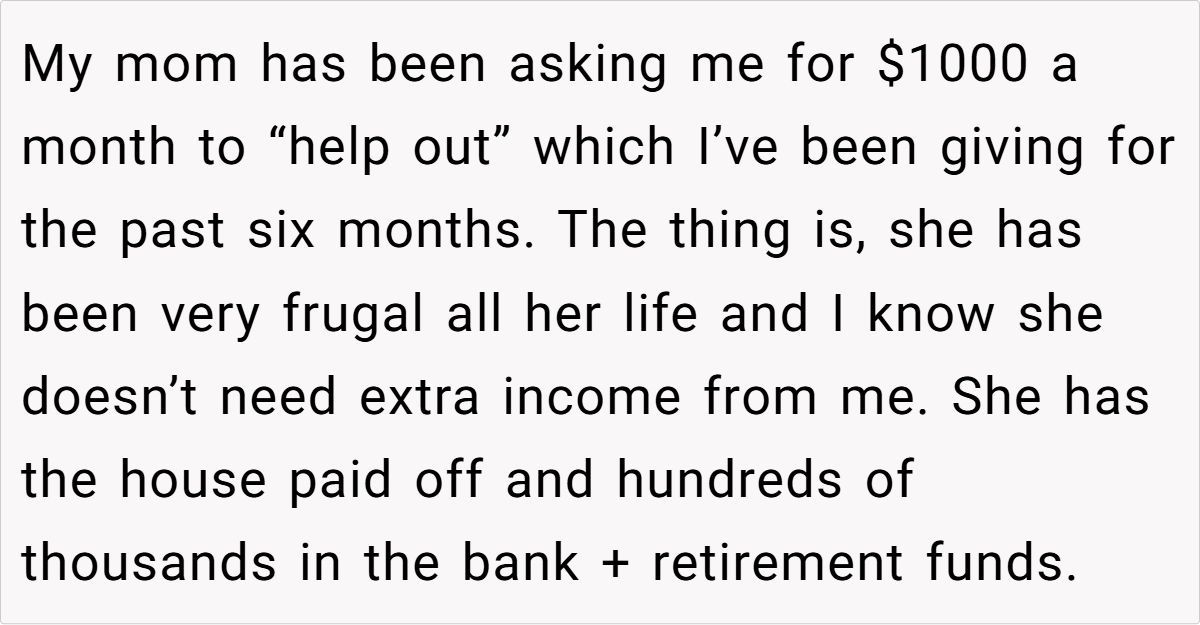

Letting a parent rely on you for financial support can feel like a double-edged sword, especially when the support is not driven by genuine need. In this case, the young woman’s dilemma highlights the conflict between familial duty and the rational management of personal finances. Her mom’s request appears less about practical assistance and more about showcasing her child’s success.

This dynamic can place undue pressure on the provider, potentially compromising long-term financial goals and personal freedom. The situation underscores the importance of establishing clear boundaries when money and family intertwine.

Diving deeper, we observe that the mother’s insistence on receiving money isn’t merely about cash flow—it’s about maintaining a certain image among her peers. With a house paid off and substantial savings at her disposal, her desire for a monthly allowance is rooted in pride and the need for validation.

Such behavior is not uncommon; many parents subconsciously equate their children’s success with their own self-worth. However, when financial contributions become a tool for ego-boosting rather than practical support, the giver may feel exploited rather than appreciated.

From a financial perspective, handing over $1,000 monthly when you could be investing that money for your future is a significant opportunity cost. The interest and potential growth from even a high-yield savings account or a diversified portfolio could far outweigh the fleeting satisfaction of a parent’s bragging rights.

It is crucial to weigh the emotional guilt against the tangible benefits of building a secure financial future. In many cases, setting boundaries not only preserves financial health but also fosters healthier, more balanced family relationships.

Financial expert Suze Orman has often stressed the importance of protecting your financial well-being, remarking, “You must live for yourself first; when you’re constantly giving away your hard-earned money to prop up someone else’s ego, you compromise your future”.

Her words resonate here, suggesting that emotional obligations should not eclipse rational decision-making. When financial support is demanded for reasons other than genuine need, it’s wise to reconsider and realign priorities—ensuring that personal stability is not sacrificed for the sake of familial expectations.

Ultimately, the crux of this issue is about balance: the need to honor family while also safeguarding one’s own future. The advice is not to abandon your parent in a time of need, but rather to engage in an honest dialogue about what constitutes true support. Exploring alternative ways to show love and care—such as occasional contributions tied to specific needs or shared expenses—might be a healthier solution.

Open communication and perhaps even professional financial counseling can help both parties understand and respect these boundaries, ensuring that familial bonds remain strong without undermining financial security.

Here’s how people reacted to the post:

Many redditors jest that while money can’t buy love, it sure seems to buy a lot of bragging rights. They poke fun at the idea that a monthly check might be more about vanity than necessity, sparking lively debates on the true cost of familial support.

In wrapping up this complex case of financial and emotional entanglement, it’s clear that striking a balance between duty and self-care is essential. While the monthly allowance was initially seen as a simple favor, its deeper implications now call for a reassessment of boundaries and expectations.

What would you do if you were in a similar situation? Share your thoughts, experiences, and advice in the comments below—let’s explore how best to navigate the tricky terrain of family, finances, and the fine art of setting boundaries.

As daughter who had a mum who manipulative and used emotional blackmail for control in our relationship I would say start to look for somewhere else to live. It’s not OK that she is saying “After all I have done for you” as she chose to be a parent and the basics of food and shelter should be provided without you feeling like you owe her anything. I agree you should contribute to household expenses by splitting bills 50/50 and either buying your own groceries or splitting that too. However I would be concerned about you saying it’s hard for your mum to let you go, it’s not your responsibility to manage her feelings and your are your own person and need to find your own way in life. Yes still maintain a relationship but put some boundaries in place over this. My experience with my own mum was that she was very controlling and emotionally manipulative, she would guilt trip me and use the word “selfish” if I didn’t do what she wanted me to. She would give me the silent treatment, say awful things and I was constantly feeling guilty like I was a terrible daughter. As I got older and started to become more independent and she realised she could not control me the more she ramped up the guilt trip. I was 26 when I met my now husband and realised what a dysfunctional, emotionally abusive toxic relationship I had with my mum. It’s impacted my self esteem, self worth and mental health. I’m 42, live on the other side of the world and about 5 years ago she moved house and did not tell me where she was living, only contacting me by text so that was the nail in the coffin for me and I’ve not been in contact since. I’ve never ever set boundaries with my mum and she trampled all over be as a result. I’m not saying this is what your mum is doing but the signs are there and feeling like you owe your mum and it’s your responsibility to make sure she is OK is not healthy. Yes you can support her and have a good relationship but you need to have your boundaries and live your own life, I can foresee difficulties with relationships in the future if she is anything like my mum. When I became a parent I realised there’s lots of things about the way she parented I didn’t want to do, and even now as my son is 7 I still struggle falling into default mode and get into battles for control, I’m trying to break the cycle but it’s so hard when it’s entrenched from childhood. As for bragging about you looking after her I wouldn’t be comfortable with that, and as others have said I wonder if this is about control with the money. She can still say she is proud of your achievements without having to discuss financial aspects of your relationship and your job.

You’re 23, earn a decent wage and still live at home? £1k a month is cheap. It doesn’t matter whether your mum needs the money or not. If you don’t like it, move out.

YTA. Pay rent or move out – and stop calling it an allowance. It’s rent and bill contribution.

Set up a joint account and deposit the “rent” each month. Use this as an opportunity to work with your mother and teach financial intelligence. She can brag to her friends that you support her and you can be sure your money gains interest instead of dust under the floorboards.

1k a month in a HCOL area sounds cheap. So you aren’t making any interest on that money but the returns you are getting from your mom boasting about it are priceless. On top of that you will get it all back on the end.