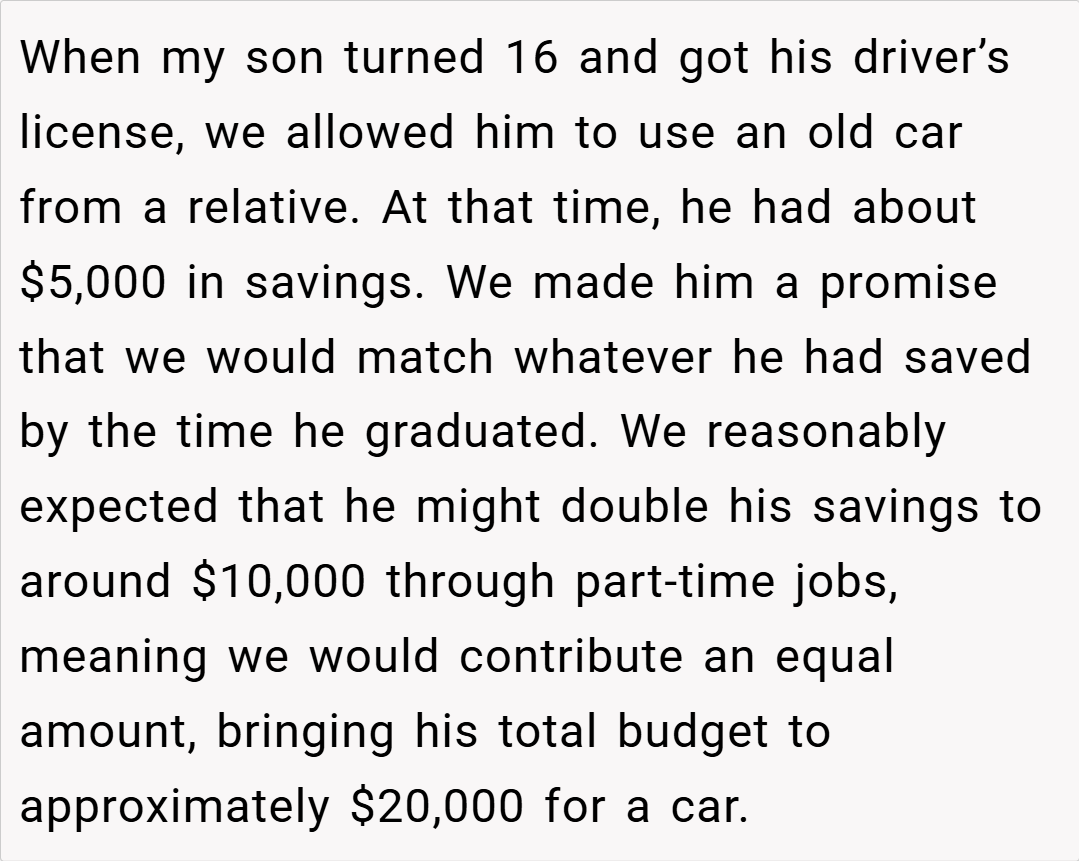

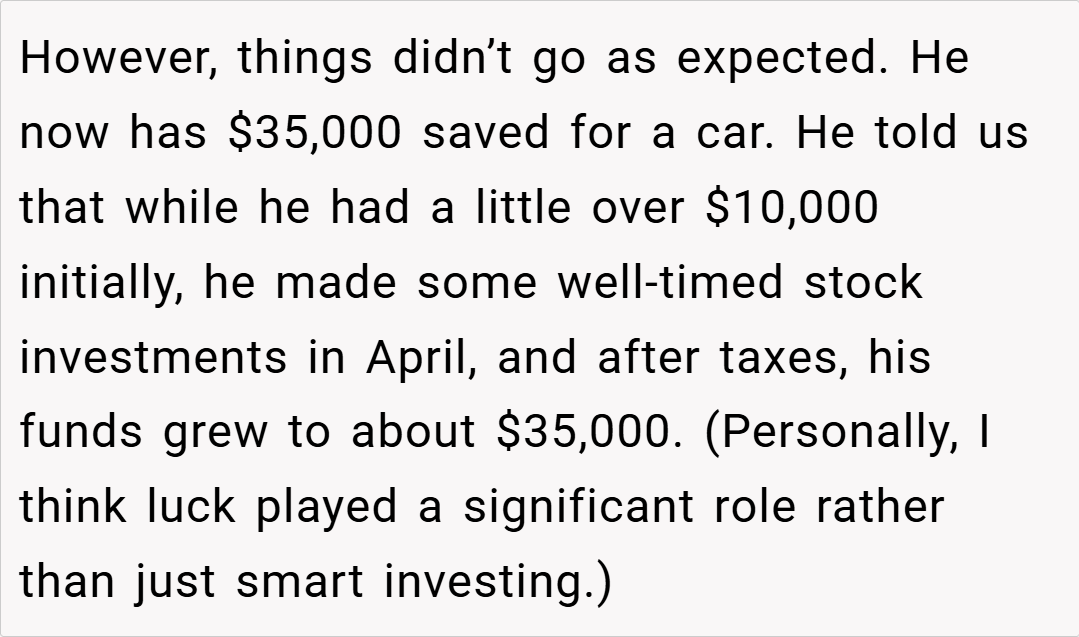

Promised My Son We’d Match His Car Savings, Now He Has More Than We Expected

A well-intentioned promise can sometimes lead to unexpected dilemmas, especially when it involves money and teenagers. One parent now faces a difficult choice after pledging to match their son’s car savings—only to find that his savings have far exceeded their expectations. Should they stick to their word, even if it means funding a car that seems excessive for an 18-year-old? Or should they adjust the agreement to reflect the spirit rather than the letter of the deal?

‘ Promised My Son We’d Match His Car Savings, Now He Has More Than We Expected ‘

Dr. Mark Ellison, a financial advisor specializing in family wealth management, says that financial promises should always come with clear boundaries to avoid unintended consequences. “The core of this issue isn’t just the money—it’s about fairness and trust. The parents made a commitment, but they also didn’t anticipate their son making such a substantial financial leap,” says Dr. Ellison.

While keeping promises is important, Dr. Ellison believes that adjustments can be made if the spirit of the agreement is honored: “If the original intent was to reward his savings efforts, the parents could cap their contribution at a reasonable amount, such as $20,000, while still recognizing his financial discipline.”

Additionally, parenting coach Linda Waters suggests that parents take this opportunity to teach financial responsibility: “Rather than just giving him $35,000, they could propose that he use part of it for a more practical car, while investing the rest for the future.”

Here’s what the community had to contribute:

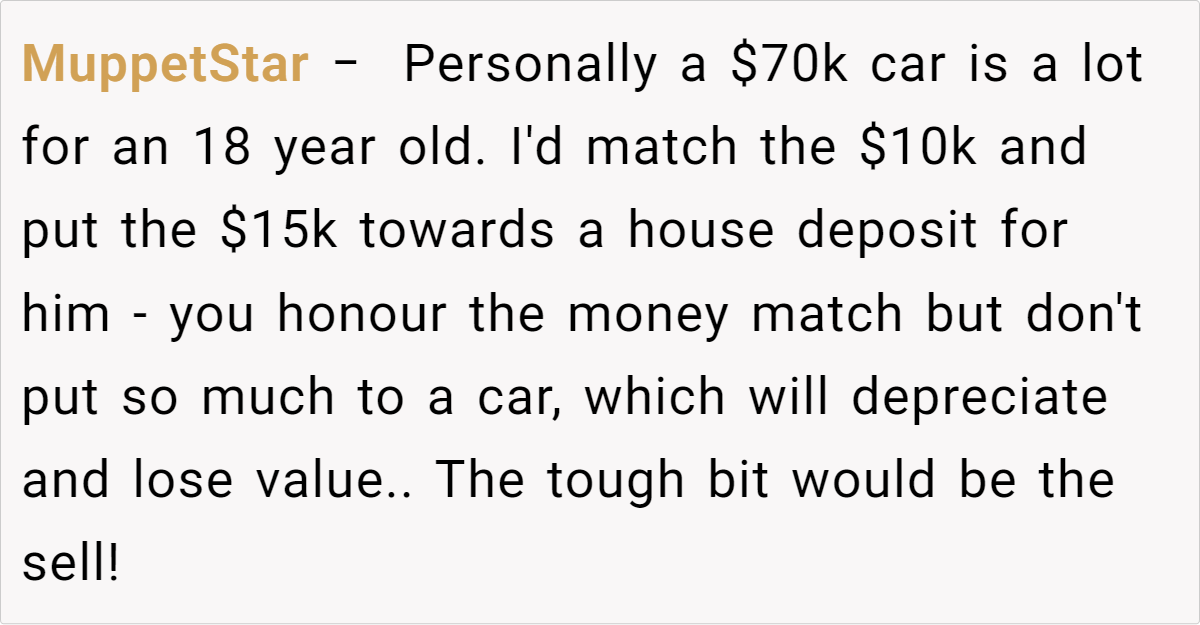

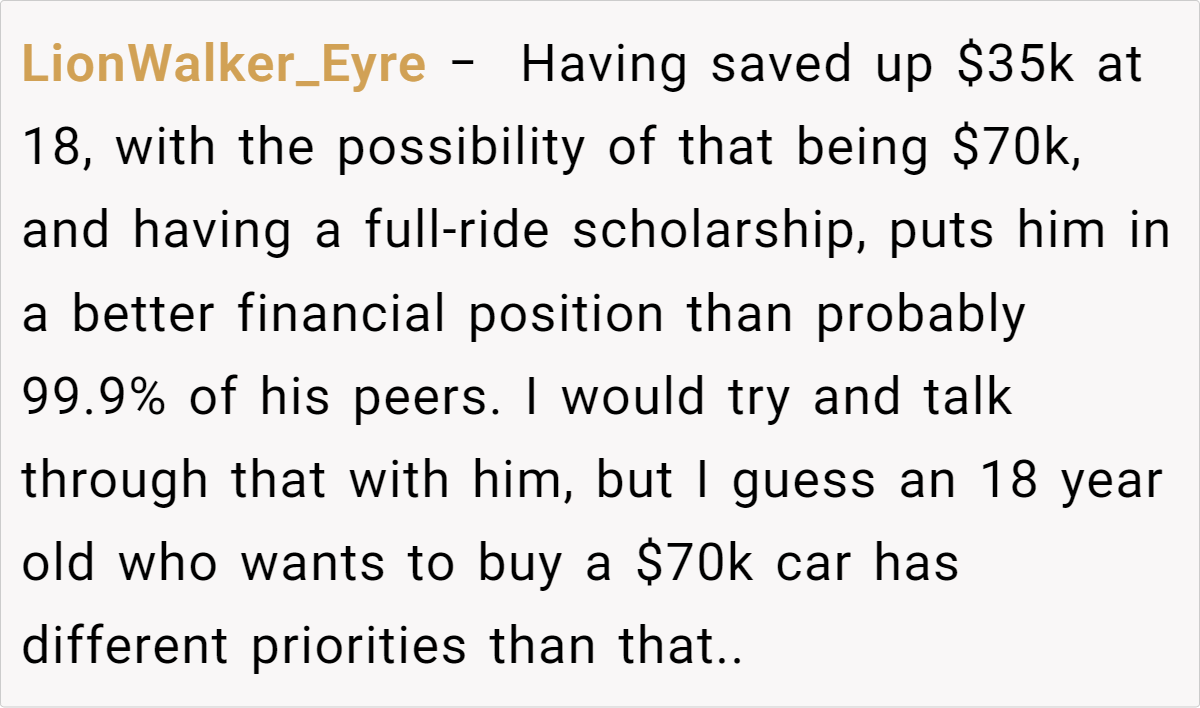

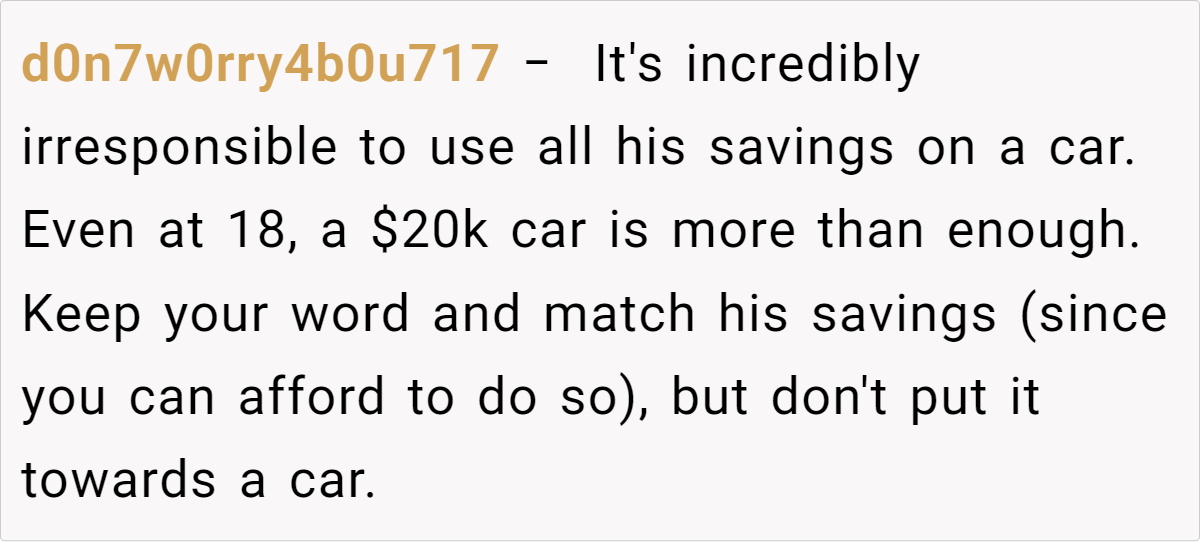

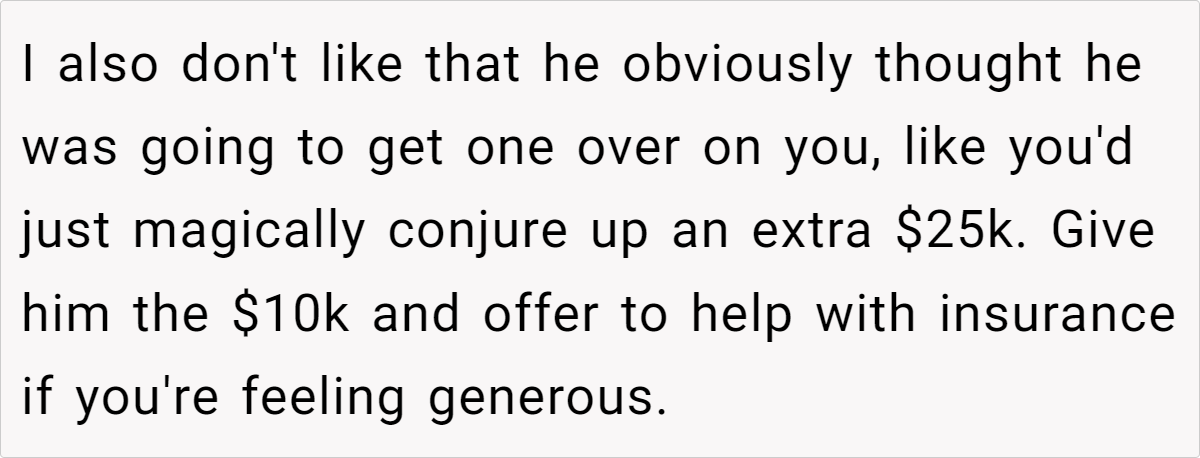

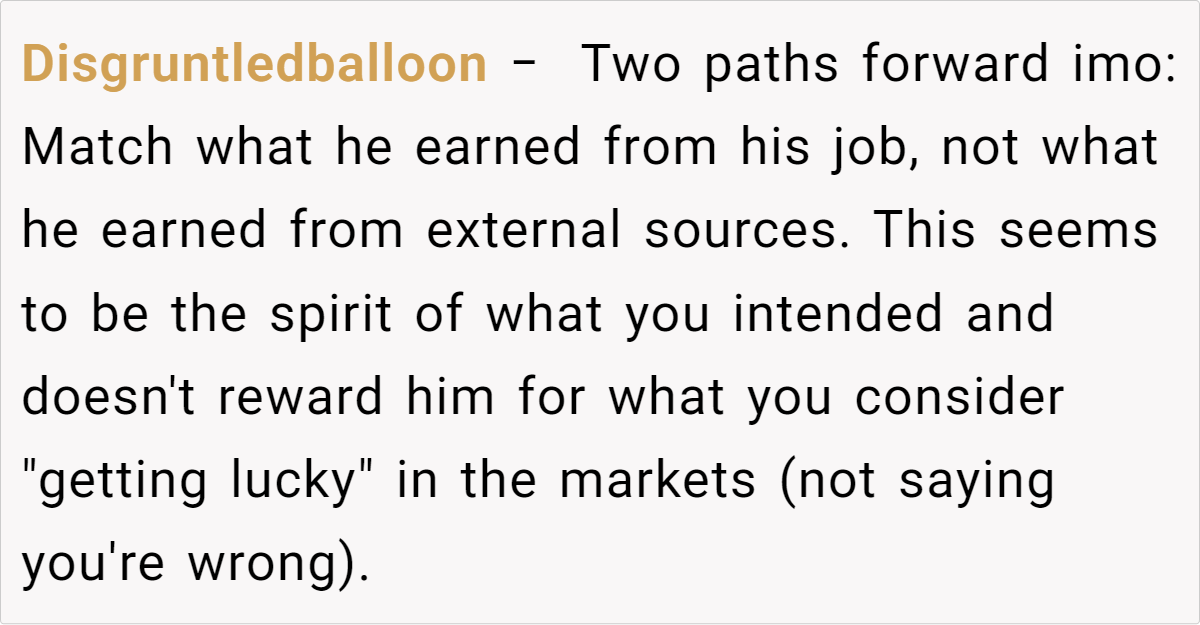

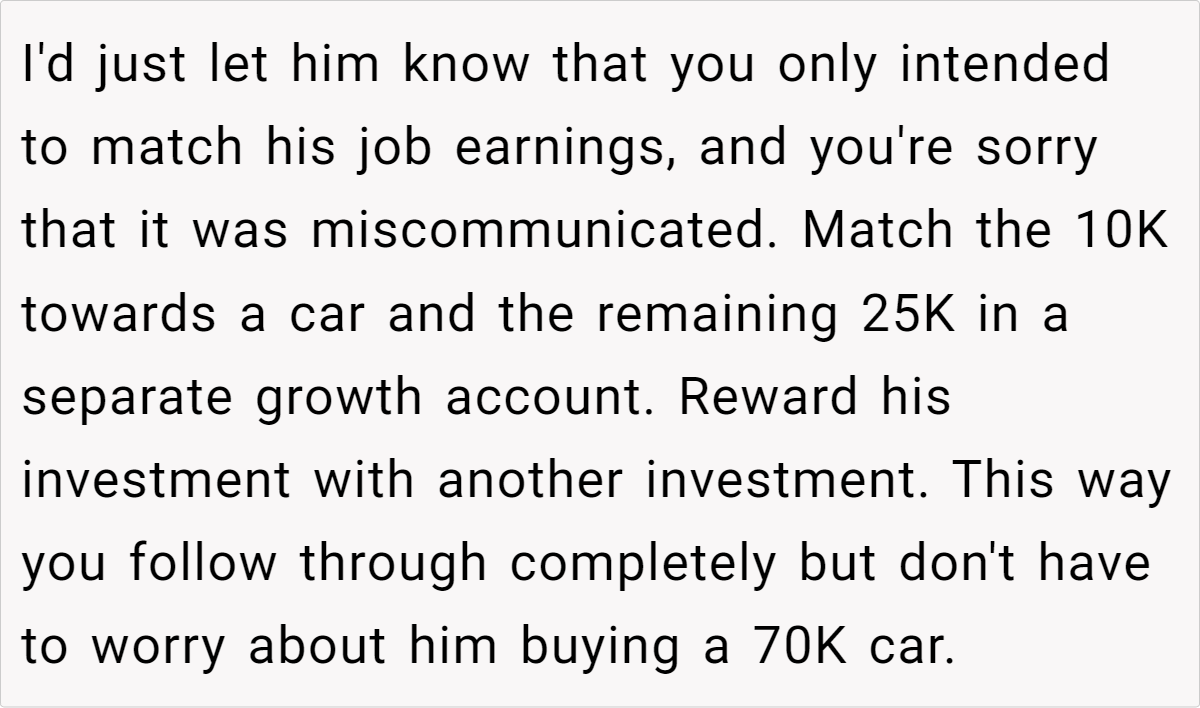

Most people agreed that sticking to the promise in some form is important to maintain trust, but that doesn’t necessarily mean handing over $35,000 in cash. Some suggested offering a reasonable cap on the contribution, while others emphasized using this as a teaching moment about long-term financial planning. Many also pointed out that an 18-year-old doesn’t need a luxury car and that the parents should guide him toward making a more responsible purchase.