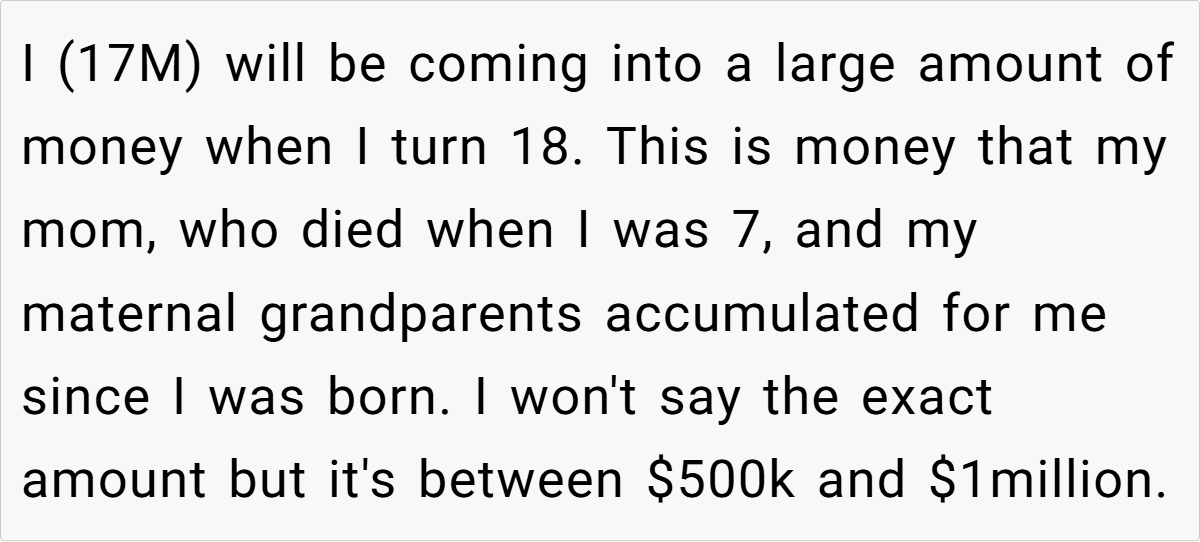

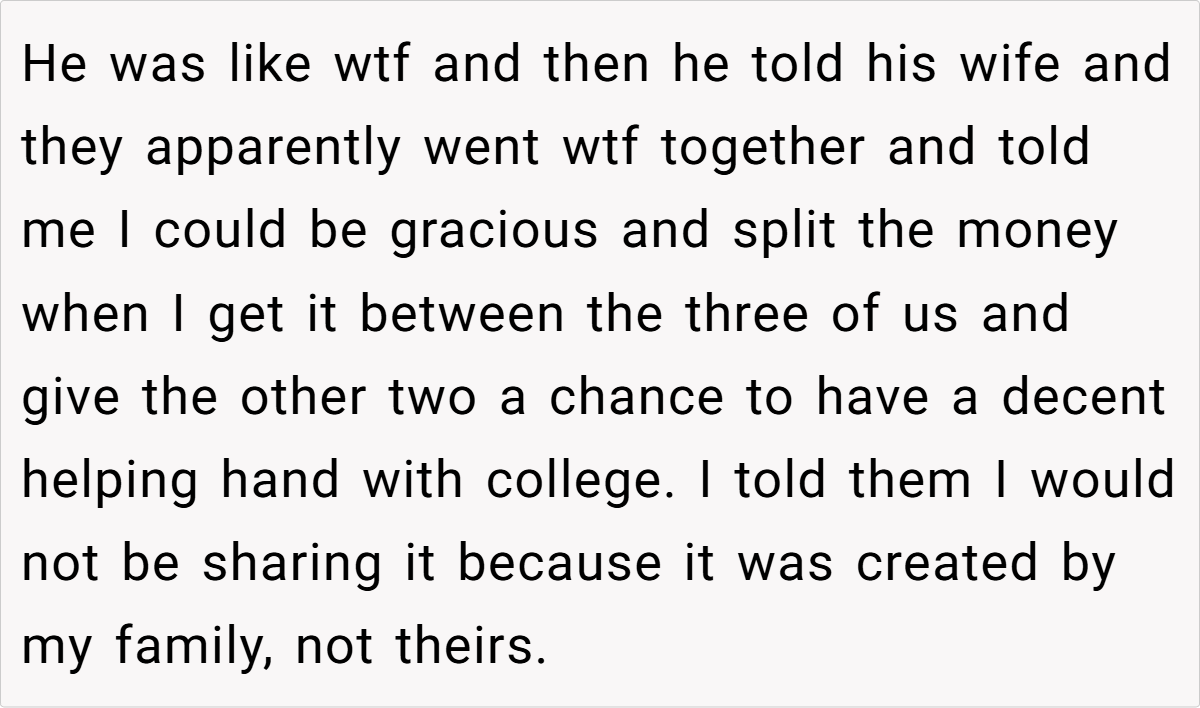

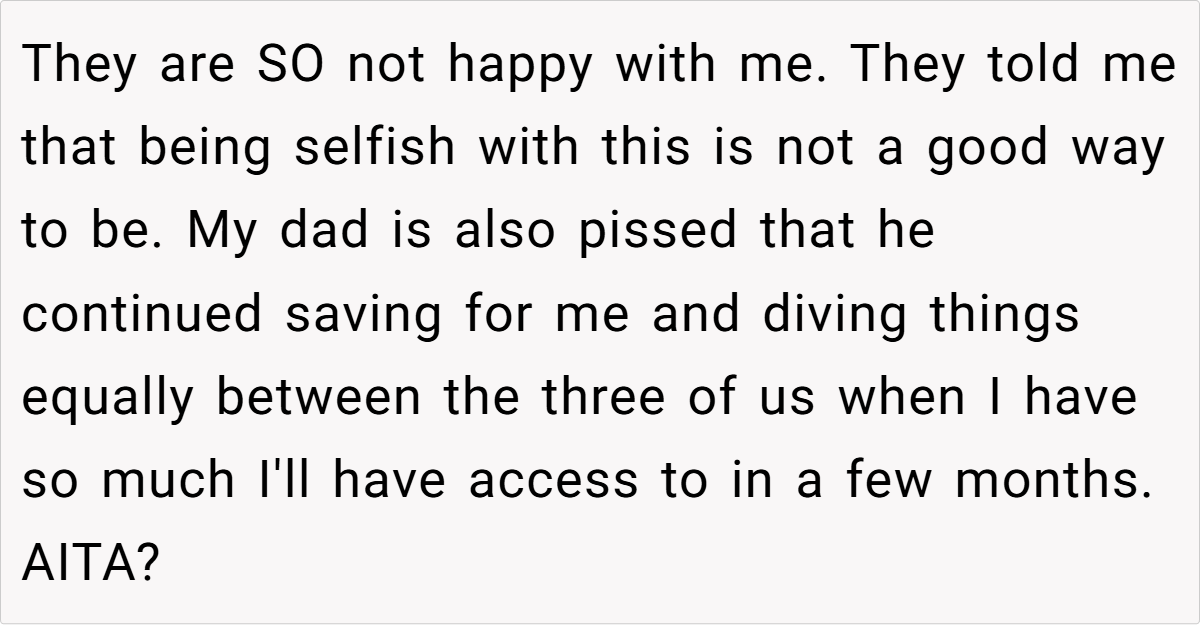

AITA for refusing to share money I will be given/have access to at 18 with my stepsister and half brother?

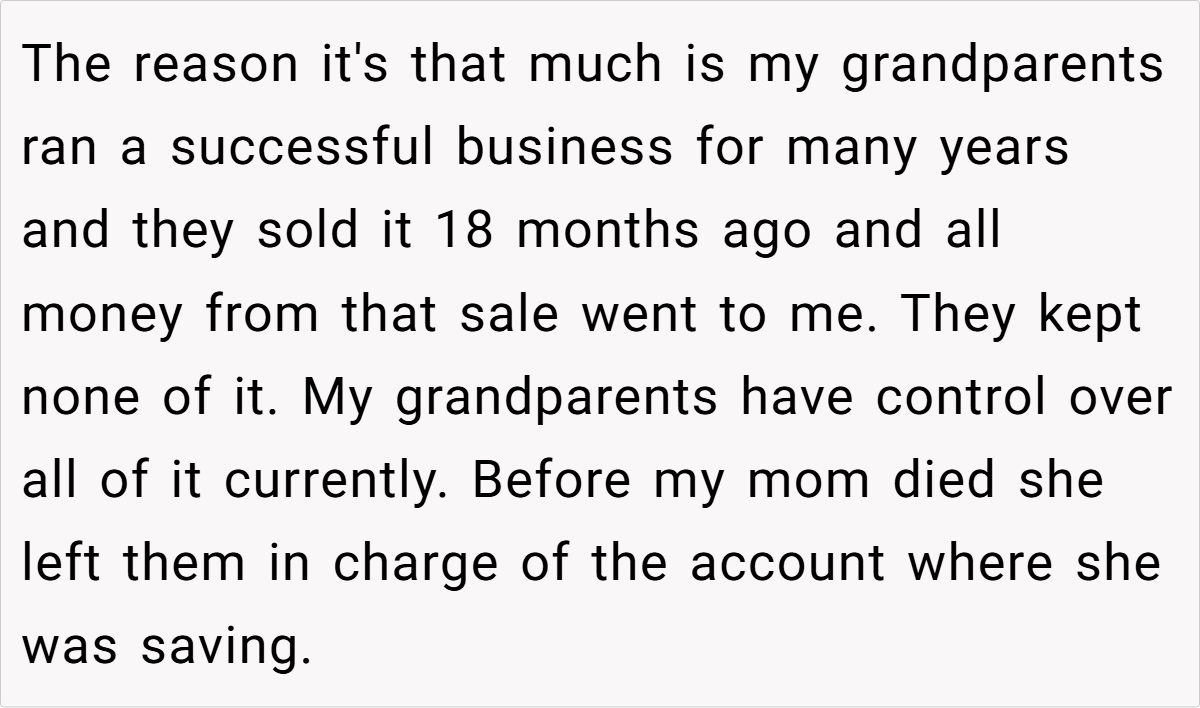

Inheritance can be as much a source of hope as it is a trigger for conflict. In one recent Reddit post, a 17‐year‑old outlines a difficult family situation: he is set to receive a large sum of money from his late mother’s savings and business sale, only to face pressure from his stepmother—and by extension, his half‑siblings—to share that windfall.

The post paints a vivid picture of familial expectations, personal boundaries, and the emotional tug‑of‑war that often accompanies inheritances. It invites us to reconsider: when money has been carefully saved by loved ones for a child’s future, who really owns that legacy?

In today’s fast‑changing world, such conflicts challenge traditional ideas of fairness and family duty. They force us to ask tough questions about autonomy, gratitude, and responsibility. Can one truly separate the financial blessing intended for one person from the complex dynamics of a blended family? Read on as we explore this issue further, breaking down the original story, expert insights, and community reactions.

‘AITA for refusing to share money I will be given/have access to at 18 with my stepsister and half brother?’

Letting an inheritance remain solely for the child it was intended for is a sentiment echoed by many financial experts. In this case, the OP’s late mother and maternal grandparents carefully amassed a substantial sum—meant to secure his future and offer him a world of possibilities. As one trusted financial advisor notes, “When money has been set aside with a clear purpose by those who love you, it is not only financially wise but also emotionally respectful to preserve that legacy for yourself.” This expert perspective reinforces that the money was never meant to be a communal asset, especially when the intent was to protect the child from future familial disputes.

Many advisors stress the importance of a thoughtful, measured approach to sudden inheritances. They recommend taking time to plan and invest wisely, rather than yielding to family pressure that could undermine long‑term goals. “A well‑structured plan—not a hasty division—ensures that the funds are used to build a secure future, exactly as intended by the benefactors,” the advisor explains. This approach aligns with the OP’s stance: by keeping the inheritance intact, he honors his mother’s wish and safeguards the resources meant exclusively for him.

Furthermore, experts emphasize the value of clear communication. Establishing boundaries early on can help reduce misunderstandings with family members who might have different expectations. As one financial strategist puts it, “When everyone understands that the inheritance was designed to serve a specific purpose for one child’s future, it sets a respectful precedent that protects both the financial asset and family relationships.” This balanced view encourages a forward‑thinking mindset—one where careful planning and respect for personal legacy take precedence over immediate family demands.

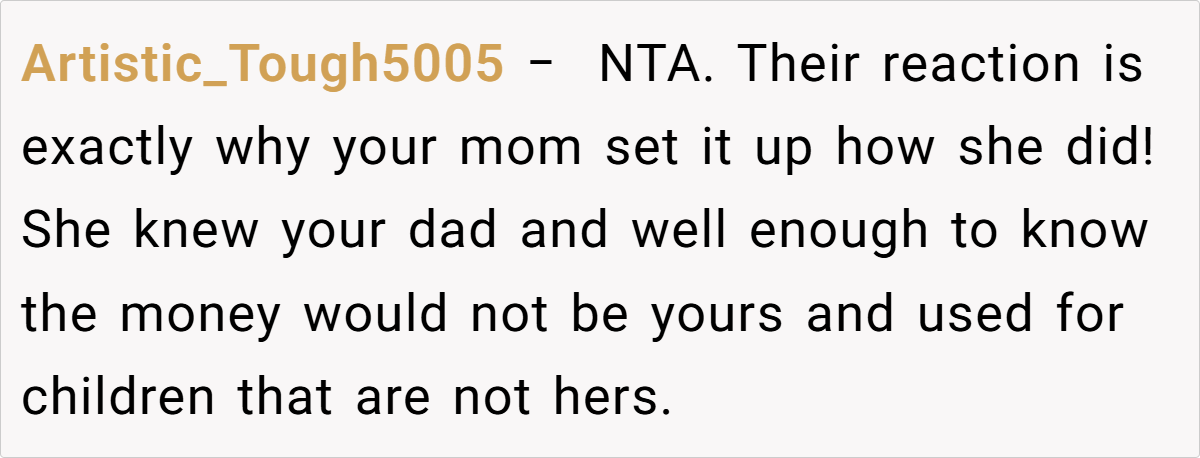

Here’s the comments of Reddit users:

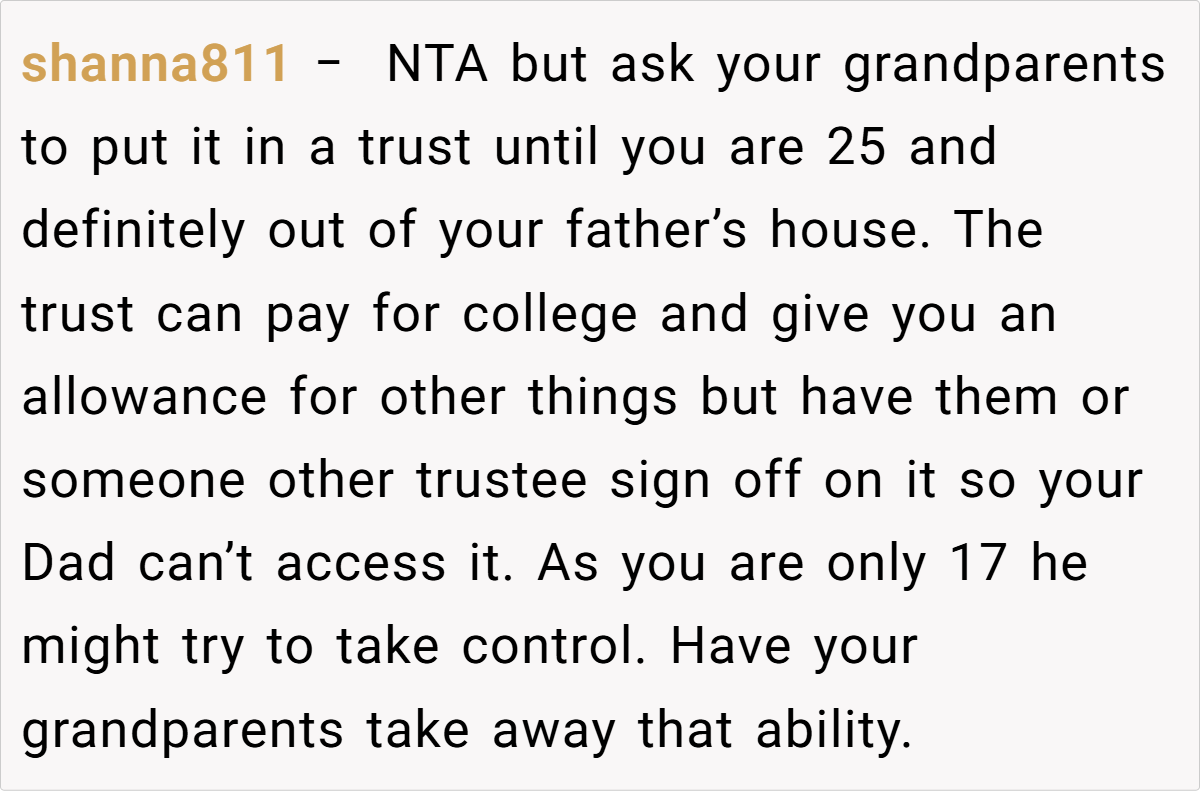

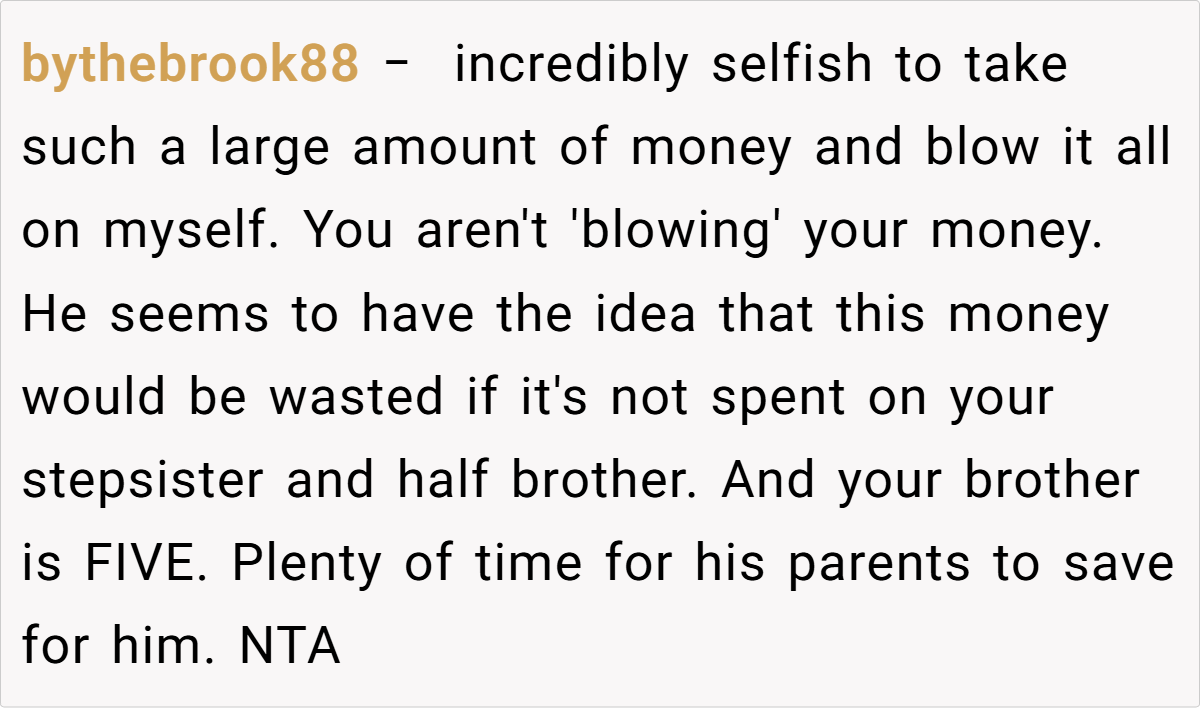

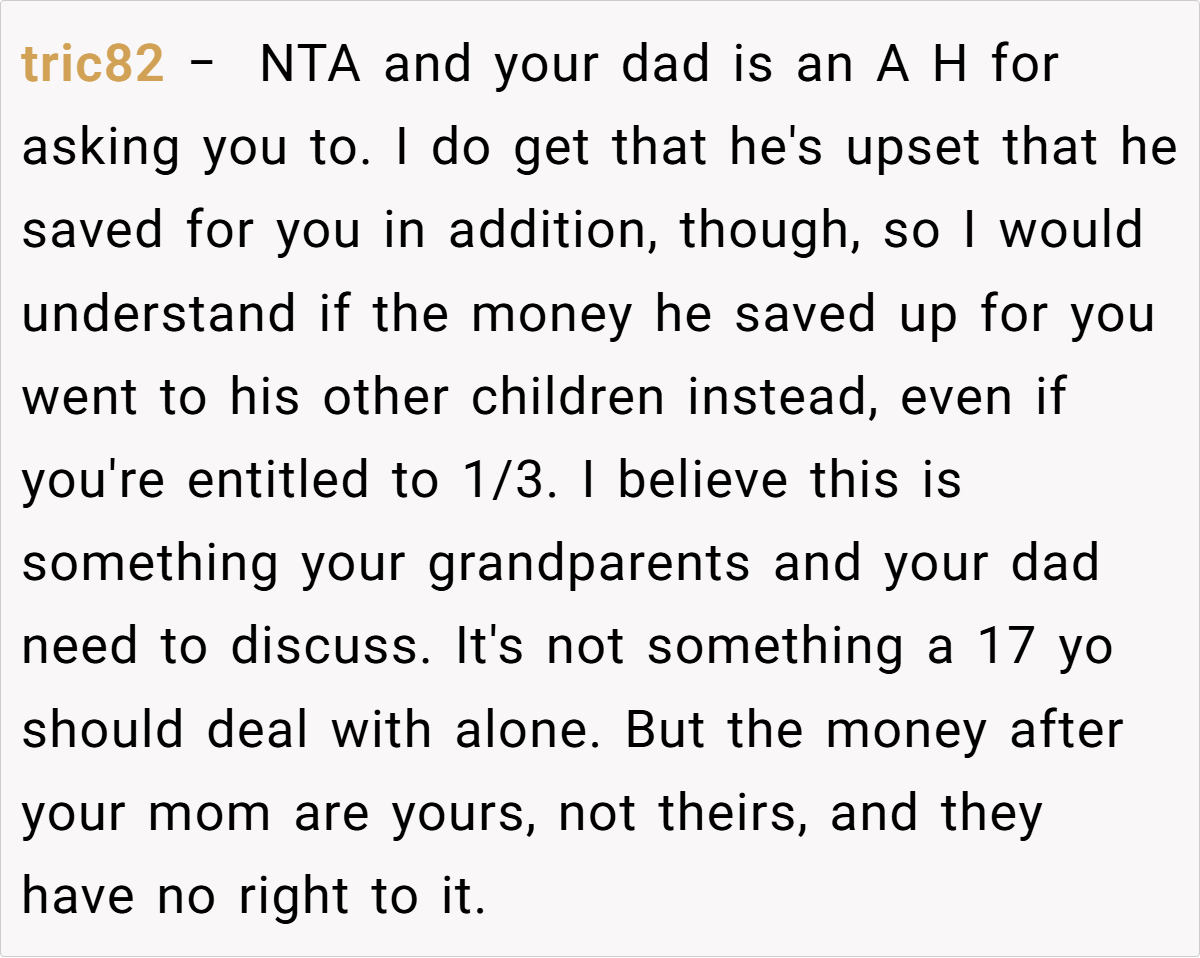

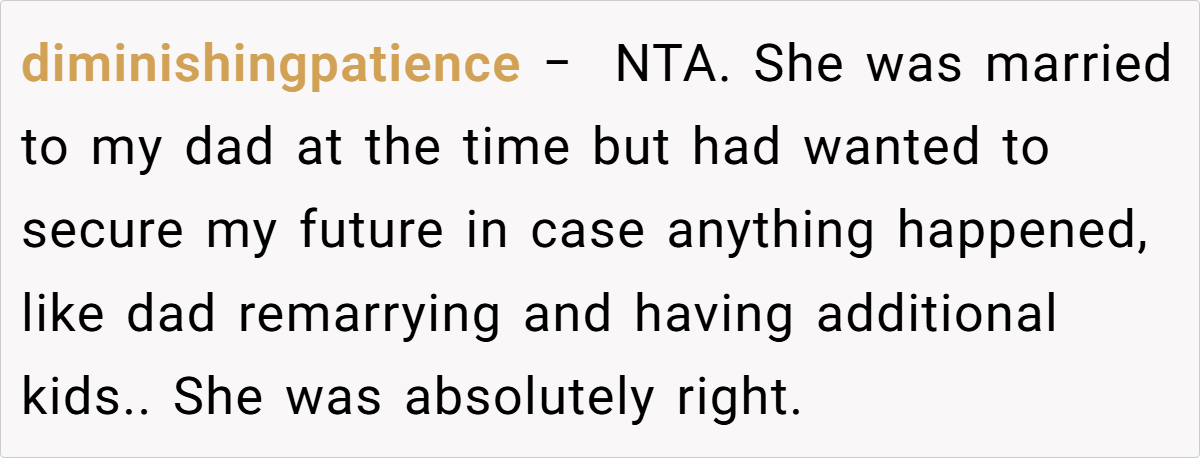

The comments emphasize that the inheritance was meant solely for you, and you have no obligation to share it with family members who weren’t originally included in your father’s plans. They advise you to protect your assets, consult with a trusted lawyer, and focus on building your own financial future rather than succumbing to family pressure.

In the end, this situation is not just about money—it’s about preserving the integrity of your future and honoring the wishes of those who set up the trust. Standing firm in your decision to keep your inheritance intact is a declaration of independence and self-respect. It invites us to reflect on our own values and the responsibilities that come with financial freedom. What would you do if you found yourself in a similar situation? Share your thoughts and join the discussion on how to balance family obligations with personal financial goals.