AITA for not letting my partner be a part of the house mortgage?

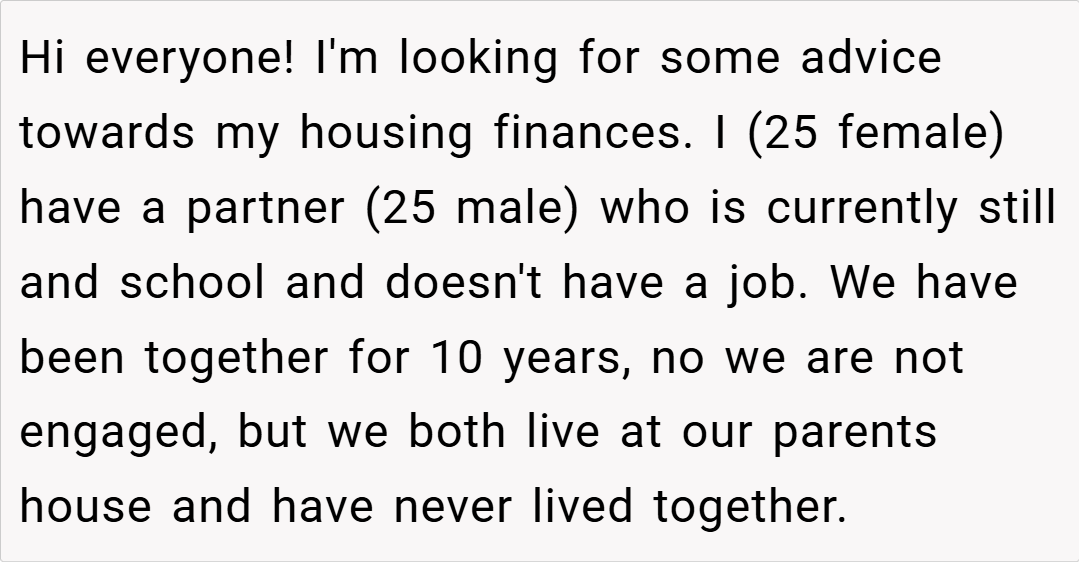

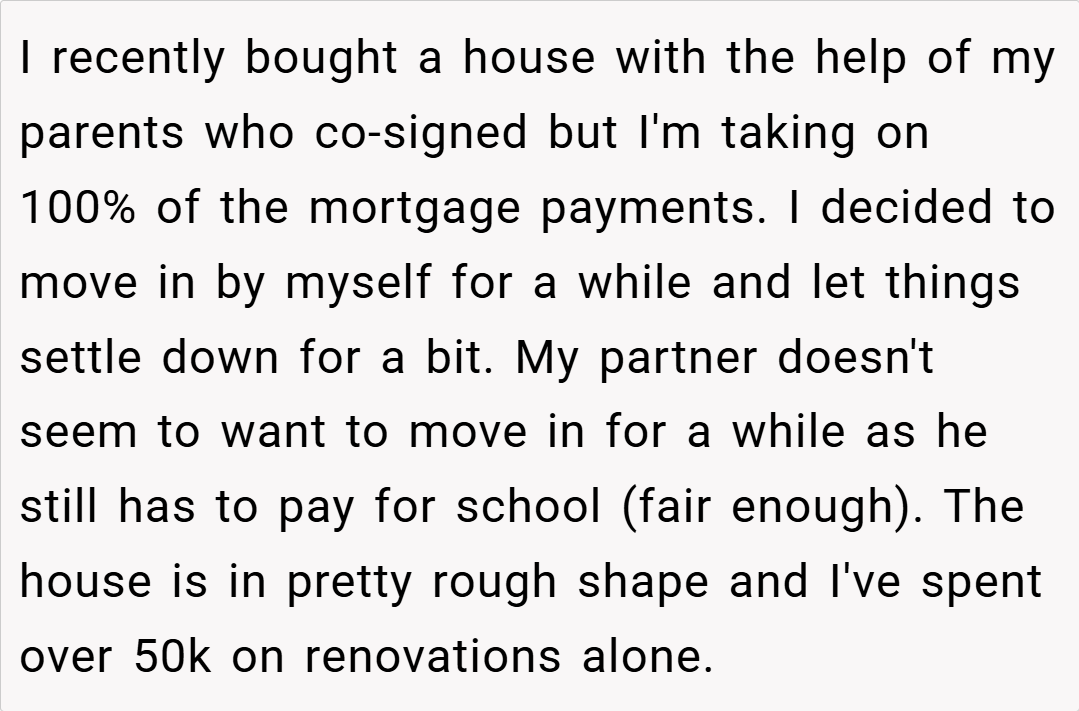

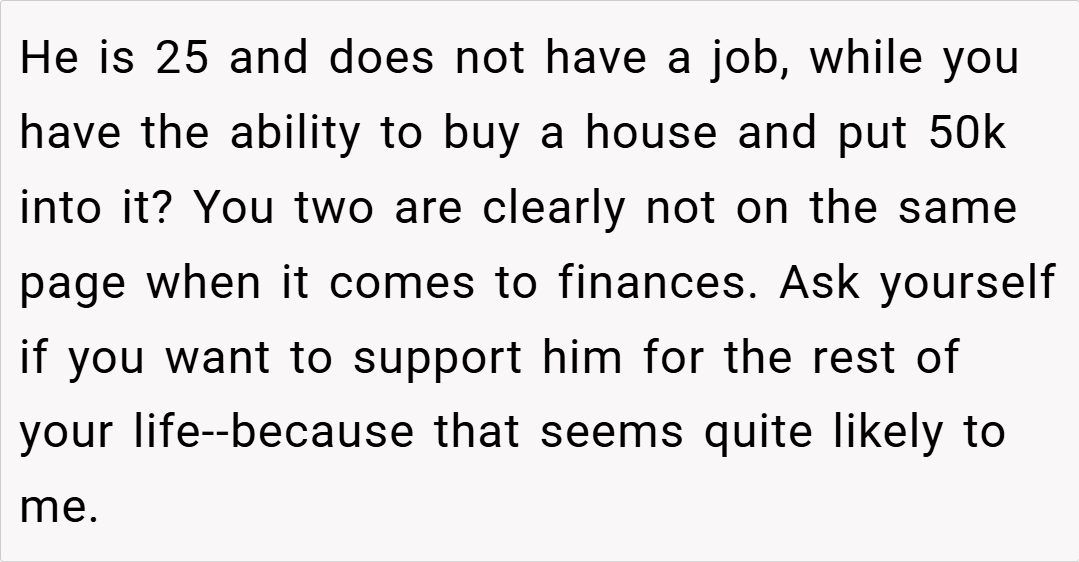

Family finances and long-term investments can be a minefield when personal relationships and expectations clash. I (25F) recently bought a house with my parents’ help—they co-signed the loan—but I’m taking on 100% of the mortgage payments. I’ve spent over $50K renovating a property in rough shape, and I decided to move in by myself for a while to let things settle.

My partner (25M), with whom I’ve been together for 10 years, is still in school and hasn’t been keen on moving in yet. However, his family is furious that his name isn’t on the mortgage, arguing that he should share in the investment to protect his future in case we break up.

‘ AITA for not letting my partner be a part of the house mortgage?’

Dr. Laura Markham, a clinical psychologist specializing in family dynamics and financial stress, explains, “In relationships where significant investments are made by one partner, it is entirely reasonable for that person to maintain control over the asset, especially if the other partner is not yet in a position to contribute financially. The key is clear, open communication about financial boundaries and long-term goals.”

Dr. John Gottman, a relationship expert, adds, “When families impose expectations based on traditional notions of shared responsibility, it can lead to friction, particularly in modern relationships where each partner’s financial contribution may differ. It’s crucial to establish mutual agreements early on, so that both partners and their families understand that financial investments are based on current realities, not just on longstanding traditions or expectations.”

Both experts emphasize that your decision is rooted in a desire to protect your financial independence and ensure that your hard work is not undermined by assumptions about future obligations.

Here’s what people had to say to OP:

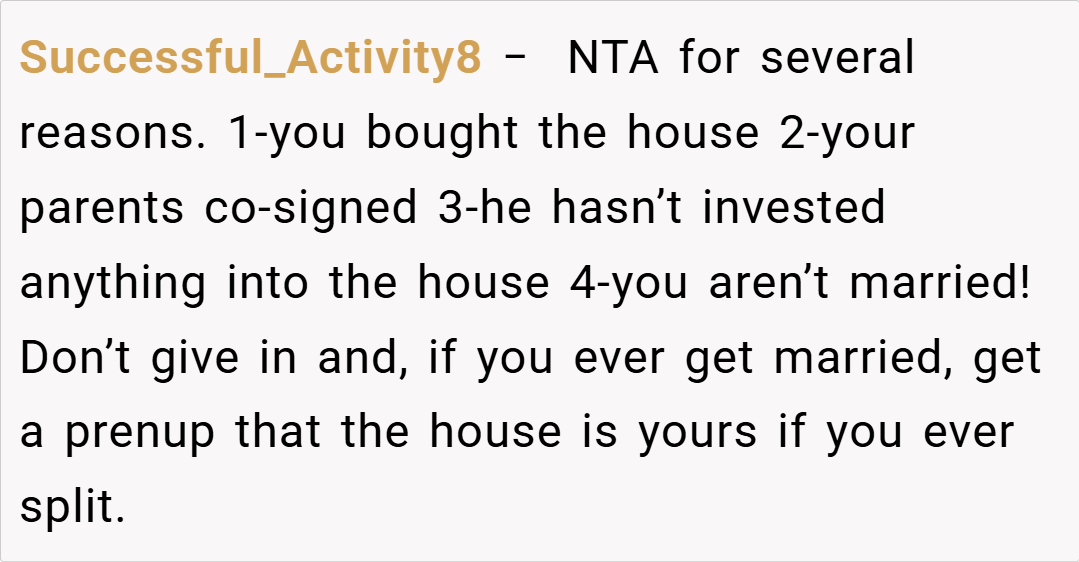

Several redditors expressed support, with one user commenting, “If you’re the one paying all the bills and investing in renovations, you shouldn’t be forced to share the burden just because someone else isn’t in a financial position yet. Your partner’s family is overstepping by assuming entitlement.”

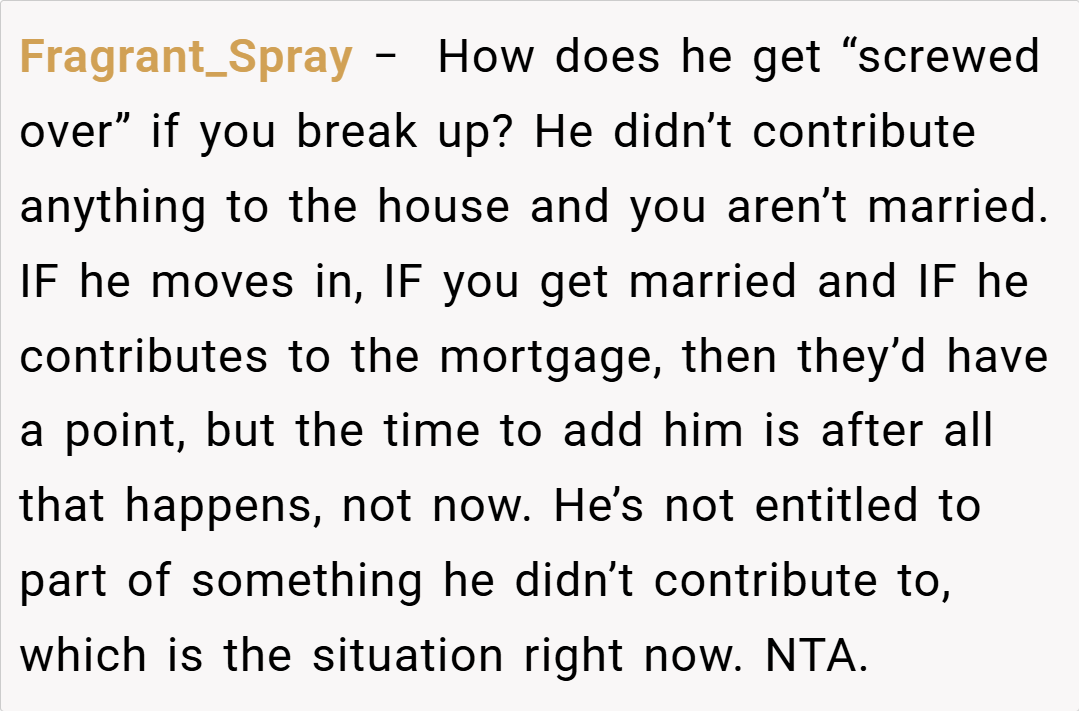

Another commenter shared, “Long-term relationships are complex, but financial contributions should be based on current circumstances. You’re not obligated to include your partner on the mortgage if he isn’t contributing, and his family should respect that.”

Ultimately, your decision not to add your partner to the mortgage reflects a practical approach to protecting your financial investment and independence. While his family’s concerns stem from traditional expectations, it’s important to remember that financial contributions should match actual earnings and current responsibilities.

This situation raises an important question: How do we balance long-term relationship expectations with individual financial realities, especially when one partner is not yet in a position to contribute?

What would you do if faced with a similar conflict between personal investment and family expectations? Share your thoughts and experiences below—your insights might help others navigate the delicate balance between personal finances and relationship dynamics.

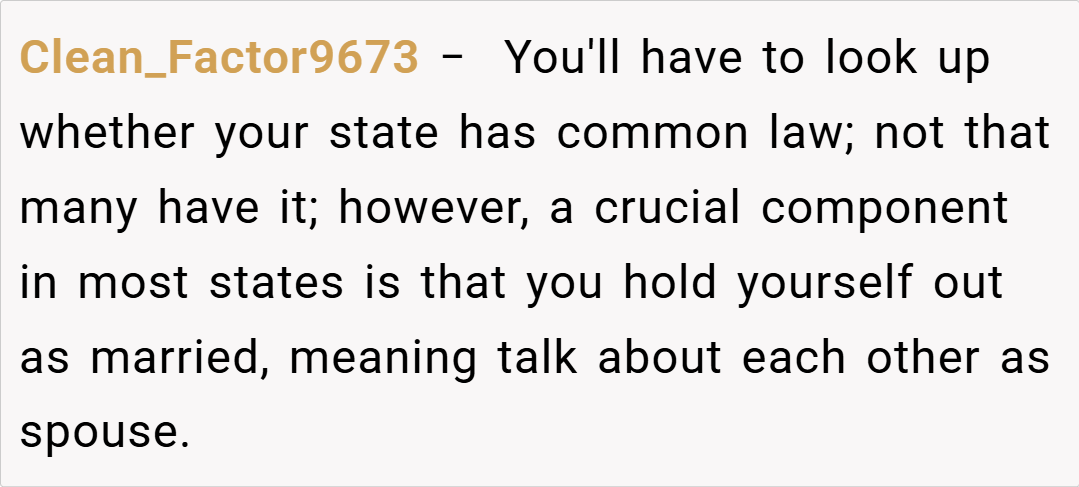

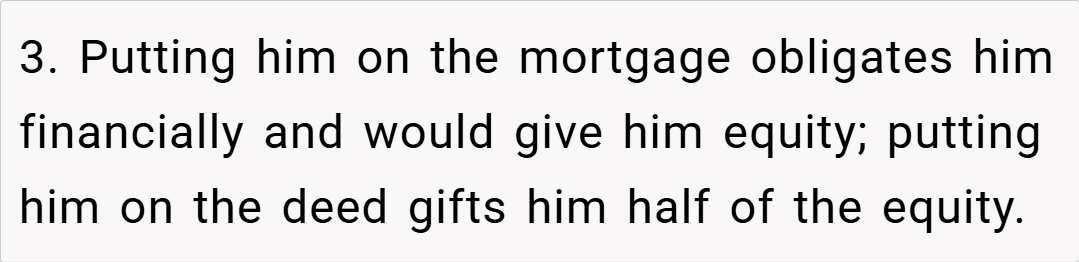

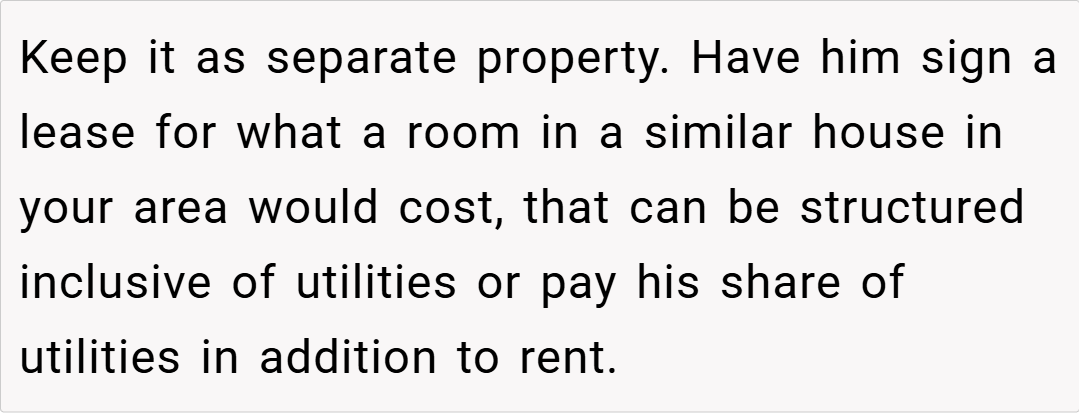

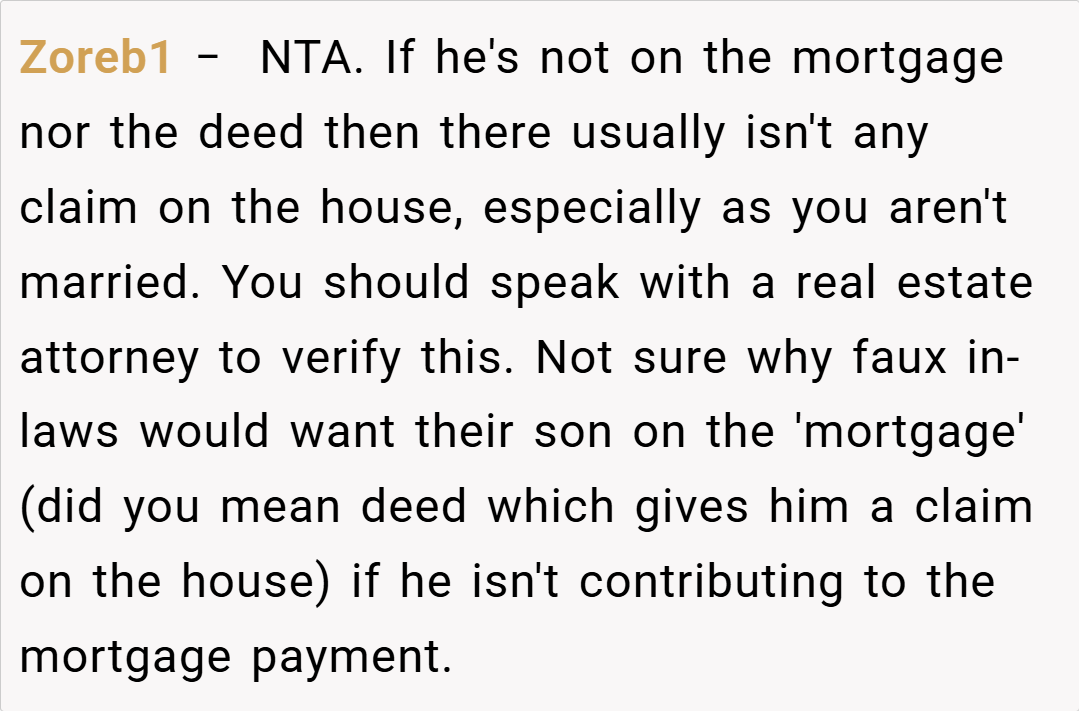

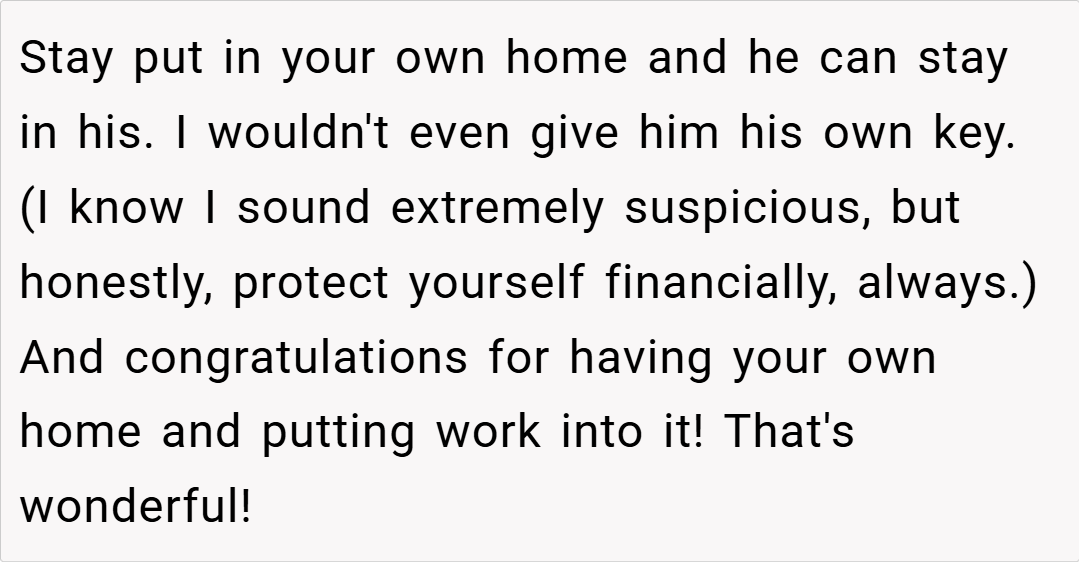

No mortgage company is going to put him on a mortgage without an income. I suspect they meant the deed. Don’t do that. That gives him half the equity in the house. It’s also none of their business.